A Step-wise Variable Cost Can Be Separated Into a Fixed Component and a Variable Component.

Toll behavior patterns

In that location are four basic cost behavior patterns: fixed, variable, mixed (semivariable), and stride which graphically would announced as beneath.

The relevant range is the range of production or sales book over which the assumptions about toll behavior are valid. Often, nosotros describe them equally fourth dimension-related costs.

A graph depicting the relevant range would look like this:

Fixed costs remain abiding (in total) over some relevant range of output. Depreciation, insurance, holding taxes, and administrative salaries are examples of fixed costs. Recall that then-called fixed costs are fixed in the curt run just not necessarily in the long run.

For example, a local loftier-tech company did not lay off employees during a contempo decrease in business volume considering the management did non desire to hire and railroad train new people when business organization picked up once more. Management treated direct labor every bit a stock-still price in this situation. Although volume decreased, directly labor costs remained fixed.

In dissimilarity to fixed costs, variable costs vary (in total) directly with changes in book of product or sales. In detail, total variable costs change equally full volume changes. If pizza product increases from 100 10-inch pizzas to 200 x-inch pizzas per twenty-four hour period, the amount of dough required per 24-hour interval to make ten-inch pizzas would double. The dough is a variable cost of pizza product. Direct materials and sales commissions are variable costs.

Direct labor is a variable cost in many cases. If the total direct labor toll increases every bit the volume of output increases and decreases as volume decreases, direct labor is a variable cost. Piecework pay is an excellent case of direct labor every bit a variable cost. In addition, directly labor is frequently a variable price for workers paid on an hourly basis, as the volume of output increases, more than workers are hired. However, sometimes the nature of the work or management policy does not allow direct labor to change as volume changes and direct labor tin can exist a fixed cost.

Mixed costs have both fixed and variable characteristics. A mixed price contains a fixed portion of cost incurred even when the facility is idle, and a variable portion that increases directly with book. Electricity is an instance of a mixed cost. A company must incur a certain cost for basic electrical service. Every bit the company increases its volume of activity, it runs more machines and runs them longer. The business firm as well may extend its hours of operation. As activity increases, so does the cost of electricity.

Managers ordinarily separate mixed costs into their stock-still and variable components for decision-making purposes. They include the fixed portion of mixed costs with other stock-still costs, while assuming the variable role changes with volume. Nosotros will look at ways to split up fixed and variable components of a mixed price later in the affiliate.

A step cost remains constant at a certain fixed amount over a range of output (or sales). And then, at certain points, the step costs increase to higher amounts. Visually, step costs announced like stair steps.

Supervisors' salaries are an case of a pace cost when companies hire additional supervisors as production increases. For example, the local McDonald's eatery has one supervisor until sales exceed 100 meals during the lunch hour. If sales regularly exceed 100 meals during that hour, the company adds a second supervisor. The supervisor costs will remain the same for betwixt 0 – 100 meals served that hour. When meals served are between 101 – 200, the supervisor price goes upward to reflect ii supervisors. Step costs will increment past the aforementioned amount for each new cost or step. Step costs are sometimes labeled as step variable costs (many modest steps) or pace fixed costs (only a few large steps). In graph form, a footstep cost would announced equally:

Although we have described four dissimilar toll patterns (fixed, variable, mixed, and step), nosotros simplify our discussions in this chapter by assuming managers can separate mixed and footstep costs into fixed and variable components using cost estimation techniques.

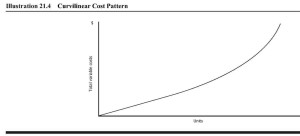

Many costs do non vary in a strictly linear relationship with volume. Rather, costs may vary in a curvilinear design—a 10% increment in volume may yield an eight% change in total variable costs at lower output levels and an eleven% change in total variable costs at higher output levels. Nosotros bear witness a curvilinear toll pattern beneath.

One style to deal with a curvilinear cost pattern is to assume a linear relationship between costs and book inside some relevant range. Within that relevant range, the total toll varies linearly with volume, at least approximately. Exterior of the relevant range, we presume the assumptions about price behavior may be invalid.

Costs rarely behave in the simple way that would make life easy for conclusion makers. Even within the relevant range, the causeless cost behavior is normally only approximately linear. As decision makers, we have to live with the fact that price estimates are non as precise every bit concrete or applied science measurements.

Source: https://courses.lumenlearning.com/managacct/chapter/cost-behavior-vs-cost-estimation/

0 Response to "A Step-wise Variable Cost Can Be Separated Into a Fixed Component and a Variable Component."

Post a Comment